We would consider the relevant range to be between one and eight passengers, and the fixed cost in this range would be \(\$200\). If they exceed the initial relevant range, the fixed costs would increase to \(\$400\) for nine to sixteen passengers. This is the net amount that the company expects to receive from its total sales. Some income statements report net sales as the only sales figure, while others actually report total sales and make deductions for returns and allowances.

Contribution margin definition

All of our content is based on objective analysis, and the opinions are our own. Now that you are familiar with the format of the CVP/Contribution Margin analysis, we’ll be using it to perform a number of what-if scenarios, but first, check your understanding of the contribution margin. The same percentage results regardless of whether total or per unit amounts are used. Assets received in a conditional contribution should be accounted for as a refundable advance until the conditions have been substantially met or explicitly waived by the donor. Revenue is recognized on the date the condition was met; it is not recognized on the grant date. A donor-imposed condition exists when it is determinable from the agreement that a recipient is entitled to the contribution only if it has overcome a barrier.

Gross Margin vs. Contribution Margin: An Overview

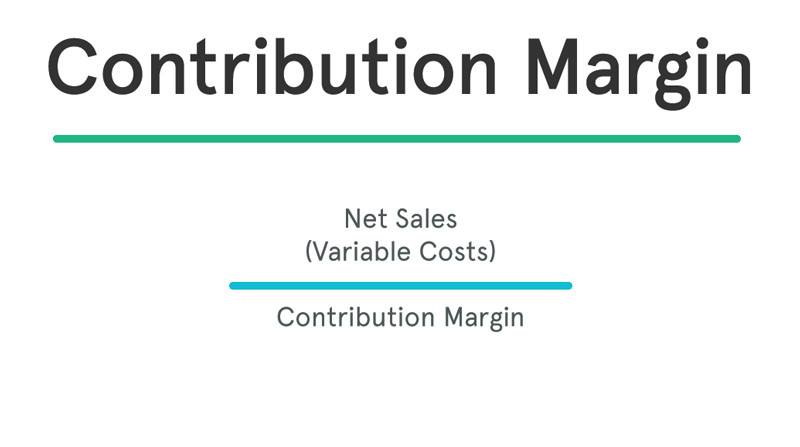

A high Contribution Margin Ratio indicates that each sale produces more profit than it did before and that the business will have an easier time making up fixed costs. A low Contribution Margin Ratio, on the other hand, suggests that there may be difficulty in covering fixed costs and making profits due to lower margins on individual sales. The contribution margin is the amount of revenue in excess of variable costs. One way to express it is on a per-unit basis, such as standard price (SP) per unit less variable cost per unit. The key difference in income statement presentation between the contribution approach and the traditional approach is that the contribution approach shifts all fixed production costs further down in the income statement. Also, if there are any variable expenses among the selling and administrative expenses (such as commissions), they are moved up in the income statement, where they are included in the calculation of the contribution margin.

Formula to Calculate Contribution Margin Ratio

One indicator in concluding whether a transfer of assets is a contribution or an exchange is that the positive sentiment from acting as a donor does not constitute commensurate value received by the resource provider. This indicator was the basis for concluding the contribution from Bravo was not an exchange. contribution definition in accounting Charlie, however, receives more than positive sentiment, such as greater visibility than Bravo and the means to promote itself and its products. Accordingly, Charlie is receiving commensurate value as the provider. ABC Foundation would thus apply Topic 606 in accounting for this transaction.

- It focuses on the returns (contribution) a business makes from each unit of product sold and whether that return is enough to allow the business to make money overall after taking account of its fixed costs.

- For example, let us consider a company where sales amount to $80,000 and variable cost is $40,000.

- Likewise, a cafe owner needs things like coffee and pastries to sell to visitors.

Many contribution agreements specify obligations of both the provider and recipient. The obligations can take various forms, such as activities consistent with the recipients’ normal operations, donor-imposed restrictions, and donor-imposed conditions. These obligations are subject to different accounting rules and therefore must be properly identified.

Why You Can Trust Finance Strategists

We’ll explore this in more depth when we talk about variable costing vs. full-absorption costing later in this module. The contribution margin ratio is expressed as a percentage, but companies may calculate the dollar amount of the contribution margin to understand the per-dollar amount attributable to fixed costs. Gross margin is commonly used as an aggregate measurement of a company’s overall profitability. The contribution margin is used by internal management to gauge the variable costs of producing each product. The concept of this equation relies on the difference between fixed and variable costs.

Whichever presentation approach is used, a company should be consistent in using the same form of presentation for all periods included in the financial statements. This contribution is conditional based on a measurable performance-related barrier. Kappa University must actually collect the entire $6 million matching contributions before it recognizes the donor’s gift as contribution revenue. ABC Foundation is dedicated to achieving gender equality and empowerment.

11 Financial’s website is limited to the dissemination of general information pertaining to its advisory services, together with access to additional investment-related information, publications, and links. The break-even point, or BEP, is the point at which the cost incurred and the revenues generated are equal. Any positive sentiment from acting as a donor does not constitute commensurate value received by the provider for purposes of determining whether the transfer of assets is a contribution or an exchange. However, when CM is expressed as a ratio or as a percentage of sales, it provides a sound alternative to the profit ratio.